Claiming R&D Tax Credits – Where to start?

Whether you’re a young start-up or an established business with a strong product development process, every little helps.

So, it makes sense to take advantage of whatever tax breaks you’re entitled to.

For companies with an active research and development (R&D) function, it can add up to thousands of pounds’ worth of expenditure.

But, perhaps surprisingly, not all businesses realise they’re eligible to claim research and development tax credits, and if they do, not everyone knows how to go about making a claim.

In this article, we will explain exactly, what the tax credits are, the criteria need to apply, who is eligible to apply and most importantly how you can apply.

Key Takeaways:

- R&D tax credits are a tax relief available for businesses that spend money on research and development (R&D), aimed at advancing the business. Any organization that spends money on R&D, or even has people associated with R&D projects, can claim 26% tax relief on corporation tax on all eligible elements of that R&D spend.

- To claim R&D tax credits, a company must show that the projects generate “original” or “challenging” output. The projects must comply with one or several of the specific conditions that determine whether a new product or technology is original or challenging.

- The process of claiming R&D tax credits is complex and time-consuming, so it is advisable to use an R&D tax credit partner. The role of the partner is to identify all R&D expenditure, to determine which elements of it are eligible for tax relief and then to submit a robust and accurate claim.

- Claims can be made retrospectively against R&D expenditure for up to two previous tax years (and potentially up to 38 months including the current tax year). Any expenditure across a group of companies, consultants, suppliers, and advisors on one or all projects is potentially eligible for tax credits.

How R&D tax credits work

Any organisation that spends money on research and development – or even has people associated with projects aimed at advancing the business – can claim 26% tax relief on corporation tax on all eligible elements of that R&D spend.

As a simple example, a company that has a large spend on R&D of which say, £50,000 is eligible for tax relief at 26% (£13,000), then that company’s corporation tax bill is, for example, £20,000. This would then be automatically reduced to £7,000 by the tax relief benefit.

All R&D expenditure across a group of companies, consultants, suppliers, advisors etc. on one or all projects is potentially eligible for tax credits.

Claims can be made retrospectively against R&D expenditure for up to two previous tax years (and potentially up to 38 months including the current tax year).

Why you may need to use an R&D tax credit partner

The process of claiming R&D tax credits is complex and time consuming, so it pays to use the knowledge and experience of someone who is familiar with the system.

Claims submitted must be both accurate and compliant, otherwise they risk being rejected. The explanatory and claim documentation associated with the R&D tax credits scheme runs to nearly 500 pages, so while it is technically possible to navigate a way through and to identify which of your R&D activities relate to which elements of the scheme is full of potential pitfalls.

The role of your R&D tax credit partner is to identify all your R&D expenditure, to determine which elements of them are eligible for tax relief and then to submit a robust and accurate claim.

What type of expenditure qualifies as R&D spend?

When you first look at how all your costs break down it might not be immediately obvious what might actually qualify as research and development expenditure.

For starters think about whether your new product or technology development projects over the last couple of years have included any of the following:

- Consultancy/contractor fees

- Materials

- Testing

- Purchase or hire of specialist test equipment

- Components

- Prototypes

- Production tooling for product verification and validation prior to release to production

- Salaries for your own staff and external workers such as subcontractors

- Software

- Utilities

- Materials ‘consumed or transformed’, such as such as chemicals, materials, batteries and certain forms of tooling.

What types of projects are eligible?

Any project which involves the development of products or services which can be shown to generate “original” or “challenging” output may qualify for R&D tax credits.

By contrast, if you’re developing a new product or service to compete with other similar goods that are already out there in the market, your project will not be classed as R&D spend.

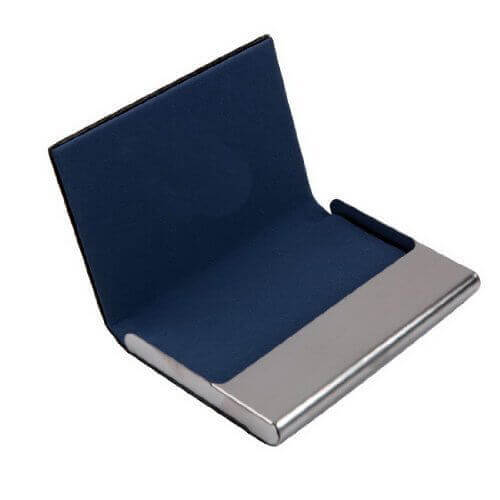

As an example, imagine a project to create a new ‘business card holder’.

Any project that sets out to develop a business card holder out of plastic or aluminium instead of stainless steel would not qualify as R&D spending on development.

However, if you are developing a completely new type of business card holder which:

- Is waterproof up to 30m

- Has blue tooth connectivity

- Automatically scans every new card you add to a Smartphone app

- Can be manufactured to retail at £4.99

…then your project would be classed as “challenging” and providing something that has never been done before.

It’s important to note that “challenging” is not necessarily “patentable”.

Your waterproof, Bluetooth-enabled business card holder may not be patentable, but as it is a new product which cannot be bought or adapted without difficulty from anywhere else for less than £5, it certainly challenges existing market norms.

What criteria determine whether a new product or technology is original or challenging?

In order for the product or technology on which you are claiming R&D tax credit to be classed as original or challenging, it must comply with one or several of a number of specific conditions by:

- Being new

- Improving existing products through technical changes

- Being patentable

- Being technically challenging to achieve

- Requiring scientific/technical research

- Being innovative

- Experimenting with new production techniques or new equipment

- Solving a set of problems which were previously unsolved

- Meeting logistical/commercial goals which were previously not achievable with available good/services

- Being capable of producing products/services more efficiently

- Having had a negative outcome – even failed project expenditure may still be eligible.

To conclude, as long as your R&D expenditure is made via your Limited Company or PLC you are eligible to claim tax credits against it. You can even claim tax credits in a loss-making scenario, which may be common when developing a new product or technology.

Please note that LLPs, sole traders and charities are not eligible to claim.

If you want to find out more about whether any of your R&D expenditure over the last 24 months may qualify for tax relief, please contact Cambridge Design Technology.

Potentially, 65% of the chargeable work undertaken by Cambridge Design Technology may be eligible for tax relief – as well as other consultancy fee expenditure, providing projects meets the criteria for R&D expenditure

Typically, SMEs get back up to 33% of the amount they’ve spent on qualifying R&D. Large companies get almost 10% back.

Here is a selection of our recent articles and case studies that you may find of interest: